Just As I Have Predicted

The Global Monetary Shift is ON

The Global Monetary Shift is ON and my crypto predictions are coming true. For years, I’ve been telling anyone who would listen: the world’s financial system is on the cusp of a seismic shift. We’re not just talking about the next “bull run” or the latest meme coin craze. I’m talking about a fundamental transformation of the global monetary system—one that is being built, right now, on the backbone of blockchain technology, digital assets, and, crucially, ISO 20022-compliant cryptocurrencies. And as we move through 2025, the facts are undeniable: the predictions I’ve made about this process are materializing before our eyes.

Let’s start with the basics. ISO 20022 isn’t some buzzword or passing fad. It’s a technical standard for financial messaging that’s being adopted by every major bank and payment provider on the planet. By November 2025, it will be the law of the land for international payments. Why does this matter? Because ISO 20022 is the bridge between the old world of clunky, slow, and expensive money movement—and the new world of instant, transparent, and programmable value transfer.

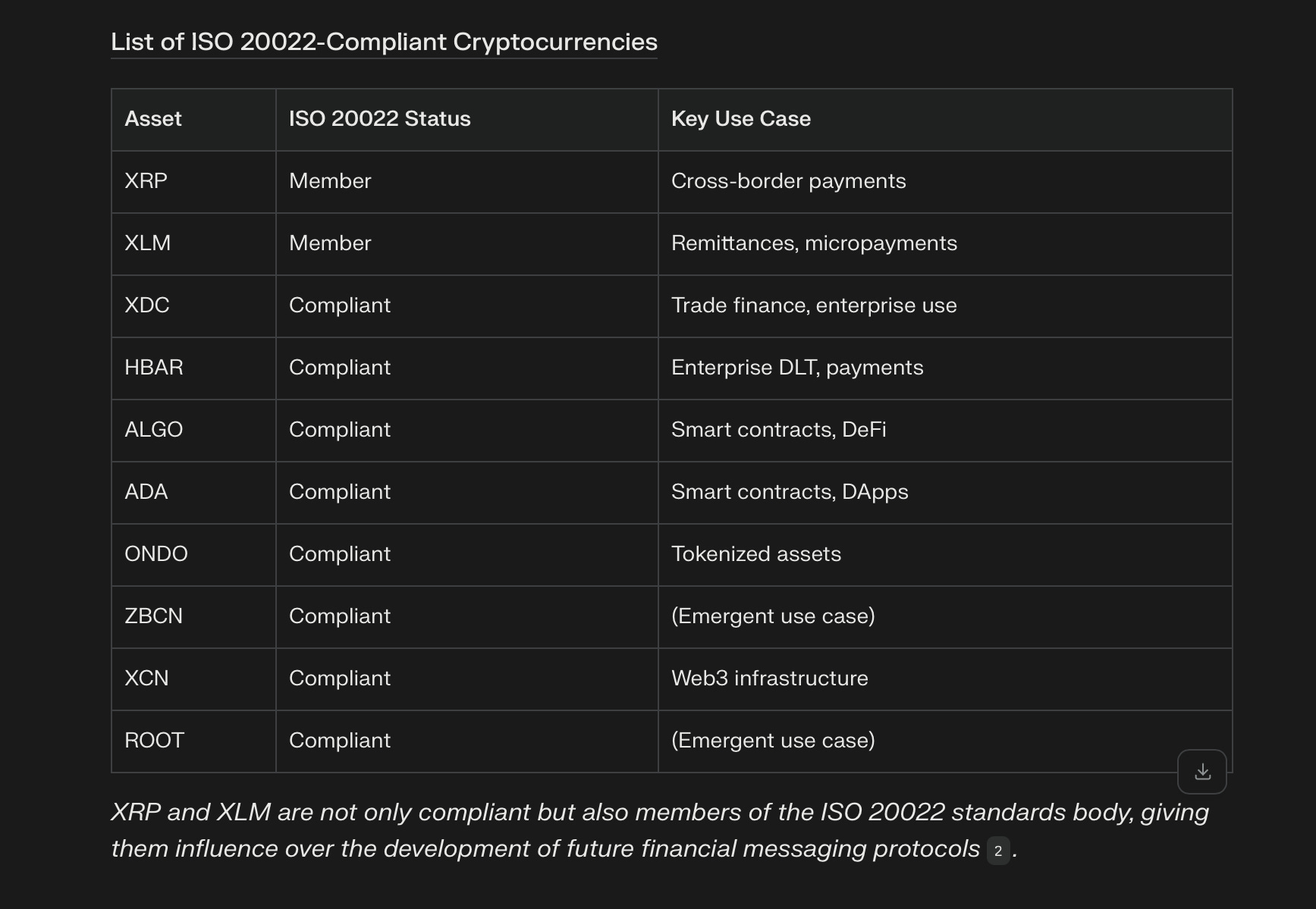

Here’s the kicker: not all cryptocurrencies are created equal. Only a select group are truly built to plug into this new infrastructure. These are the assets I’ve been pounding the table about: XRP, XLM, XDC, HBAR, ONDO, ALGO, ADA, ZBCN, XCN, and ROOT. These aren’t just coins—they’re the digital rails of the future.

Let’s talk specifics. Over the past year, we’ve seen a clear divergence in the crypto market. Meme coins and speculative tokens have had their moments, but it’s the ISO 20022-compliant assets that have shown real staying power and institutional traction.

XRP is the crown jewel here. For years, Ripple and XRP have been dismissed by some as “banker coin” or “too centralized.” But look at the facts: RippleNet is fully ISO 20022-compliant, and Ripple is now partnering with major banks and even custodians like BNY Mellon to hold stablecoin reserves. The writing is on the wall. XRP is being positioned as the bridge asset for the new global financial system.

And it’s not just XRP. XLM is making inroads in remittances and micropayments, with its ISO 20022 membership giving it a seat at the table as the new standards are set. XDC is quietly becoming the backbone of trade finance. HBAR is winning enterprise deals left and right, thanks to its speed and security. ALGO and ADA are leading the way in smart contracts and decentralized finance. Even newer names like ONDO which helps XRP and XDC in the tokenized treasury side, ZBCN(up over 45% today) which is quickly becoming the blockchain ADP, XCN which facilitates peer-to-peer lending and borrowing, and ROOT(up over 20% today) is carving out their niche in online gaming and more, all while adhering to the compliance and interoperability that ISO 20022 demands.

Upcoming Dates That Matter

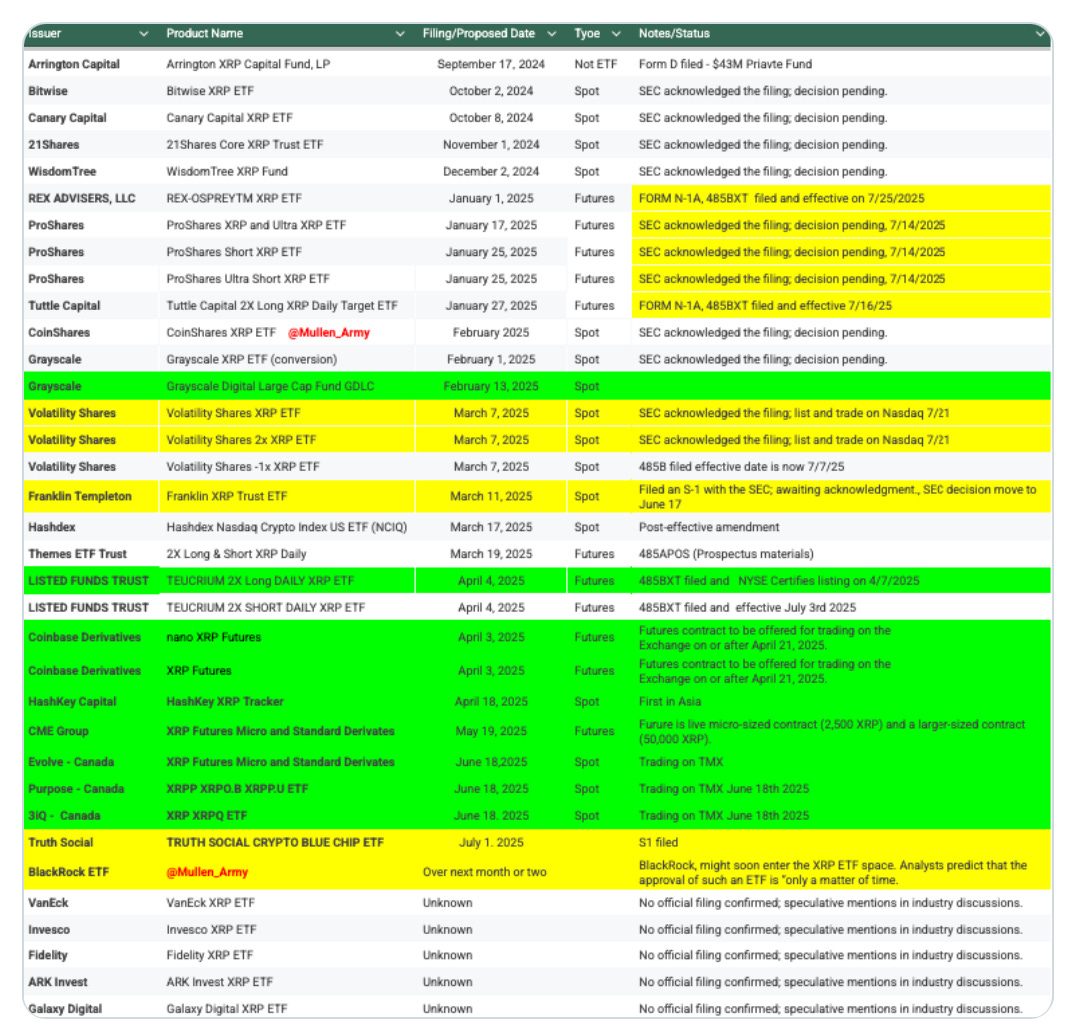

If you’ve been following my posts/calls, you know I’ve been pointing to specific dates as inflection points for this transition. Let’s zero in on XRP, since it’s the bellwether for the entire movement.

July 14, 2025: The FedWire goes live with blockchain.

July 18, 2025: ProShares ETF’s

July 16, 2025: Tuttle Capital ETF

July 21, 2025: Volatility Shares ETF

July 25, 2025: This is the date everyone should have circled. The anticipated launch of the REX-Osprey XRP ETF could be a watershed moment. If approved, it will open the floodgates for institutional money, just as we saw with Bitcoin ETFs in the past.

November 4–5, 2025: Ripple’s Swell conference in New York. Every year, this event brings major announcements—and with the ISO 20022 deadline looming, expect fireworks. New partnerships, regulatory updates, and possibly new products are all on the table.

November 2025: The big one. This is when ISO 20022 becomes mandatory for global banks. After this, the old SWIFT messaging system is officially legacy tech. XRP and its compliant peers will be the only digital assets truly ready for the new era.

For a long time, my predictions were met with skepticism. “Why would banks use crypto?” “Isn’t blockchain too slow?” “Aren’t regulations going to kill this?” But look at what’s happened just in the past 12 months. We’ve seen:

Major banks integrating with RippleNet and other ISO 20022-compliant networks.

The SEC softening its stance and greenlighting crypto ETFs, including the potential XRP ETF.

Massive inflows into compliant assets, while non-compliant coins have stagnated or faded.

Regulatory clarity emerging in the US, Europe, and Asia, all pointing toward a future where digital assets are not just allowed, but required, for financial institutions.

This isn’t just about price action or short-term gains. This is about the architecture of the next hundred years of finance. The assets I’ve been tracking are not only compliant—they’re essential. As trillions of dollars move across borders every day, the world needs assets that are fast, secure, and interoperable. ISO 20022 is the key, and the assets I’ve highlighted are the ones holding that key.

As we move through the rest of 2025 and beyond, keep your eyes on the following:

Institutional adoption: Watch for more banks, payment providers, and even governments integrating ISO 20022-compliant assets.

Regulatory clarity: Each new law or guideline is another domino falling in favor of compliant digital assets.

ETF launches and inflows: The XRP ETF could be the spark that ignites the next phase of adoption.

Network upgrades and partnerships: Every new integration is a step closer to mass adoption.

It’s one thing to make predictions; it’s another to see them validated in real time. The facts are clear: the global monetary system is changing, and it’s changing in exactly the way I’ve been describing. ISO 20022-compliant assets like XRP, XLM, XDC, HBAR, ONDO, ALGO, ADA, ZBCN, XCN, and ROOT are not just surviving—they’re thriving. The dates I’ve pointed to are proving pivotal. The world is waking up to the reality I’ve been championing all along.

If you’ve been paying attention, you’re already ahead of the curve. If not, now is the time to get educated and get positioned. The new financial system isn’t coming—it’s here. And the assets leading the way are the ones I’ve been talking about all along.

By Douglas J. Boggs, founder of "Smoke and Mirrors…and the Art of Critical Thinking" and author of “Quantum of Justice - The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall Street”. Douglas has two new books coming out in early 2025 to include: “The Psychology of Money” and “Mental Toughness for the Crypto Investor / Entrepreneur” to help guide readers through the investing world of crypto.